Time to Take Stock; It is indeed time to take stock of the performance of Ghana’s equity market for the 1st half of 2019 while looking into the 2nd half.

In our previous equity report, Finding pearls in the rough seas, we argued that depressed asset prices had led to discounts across the board and valuations are looking attractive. However, since then, earnings have disappointed with Ghana’s Equity Market and the macroeconomic backdrop has been slightly less supportive of a stock market recovery.

In addition, the liquidity crunch in the investment advisory space has weighed heavily on asset prices. As a result, local institutional investors have sold stocks with little regard to intrinsic value. Foreigners on the other hand remain risk-off as the declining gross international reserves cast more uncertainty around the Cedi’s near-term performance.

In this edition we look to unpack prevailing factors suppressing valuations and whether our positions will deliver value given the risks to the immediate outlook.

Are stocks still cheap?

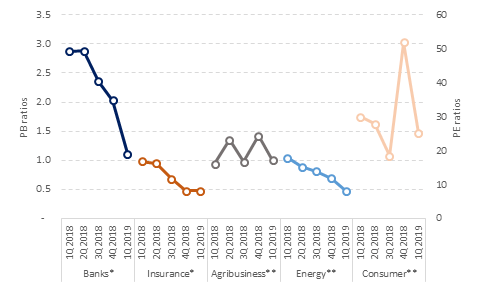

Despite weaker than estimated earnings results, share prices have declined much steeper than fundamentals. In Ghana’s Equity Market, the average price-to-book (PB) ratio for banking stocks have dropped from 2.9x to 1.1x over the last twelve months (LTM). Even on a quarter-on-quarter (q/q) basis, banks have been discounted by as much as 45.2%. Likewise, the price-to-earnings (PE) ratios for stocks in the consumer, agribusiness and energy sectors are down by an average of 27.2% from their LTM valuations presenting significant upside opportunity.

Evolution of valuation multiples across sectors

Source IC Asset Managers Research

*Valuation multiples using PB ratios

** Valuation multiples using PE ratios

In our opinion, current risks are already largely discounted, and valuations now sit below the long-term average. In effect, our positive mid- to long-term outlook for equities therefore remains unchanged.

How long will bears rule the roost?

Although Ghanaian equities are trading at discounts to their intrinsic values, we struggle to see a recovery in investor sentiments any time soon. This is because, market direction is being driven mainly by the liquidity crunch in the investment advisory space rather than fundamentals. In effect, until issues related to the repayment of locked-up investments are completely resolved, we do not believe share prices will begin to reflect fundamental valuations.

Consequently, although frontier equity markets are set to benefit from portfolio inflows on the back of another wave of global economic stimulus, we do not believe this will inure to the benefit of the Ghana Stock Exchange (GSE).

What do we do from here?

Despite the headwinds, our equity portfolio outperformed the broader market by 885 basis points (8.85%) to end the period in positive territory at 2.0%. This is a testament of how resilient our concentrated position of top picks can deliver value. That notwithstanding, we have adopted a slightly more cautious outlook due to lower than expected earnings. This is in addition to mixed corporate actions and the possibility of a protracted resolution to the impasse in the investment advisory space. We also believe that given the depth and size of the local stock market, our approach to equity investing in Ghana may require some retooling.

Private Equity

We are considering an activist private equity investing approach towards managing publicly traded equities. This is in a bid to eliminate the volatility that is associated with the local bourse. We are conducting our research and development and over the course of ensuing months, we will engage our clients on our findings and together chart a more stable path to unlocking value from Ghanaian equities.

Derrick Asare Mensah

Derrick is the Portfolio Manager, Equities. IC Asset Managers

{kind=link}