Much has been said about the value of your pension and how much you can receive as income during retirement. It is always good to refresh on the design of the scheme and to know how that plays in this discussion. First we look at the two main designs of pension schemes; Defined Benefit (DB) and Defined Contribution (DC). The level of pension received under DB depends on the level of contributions and a standard set of qualifying conditions. However, the level of pension benefits received under the DC is directly related to your level of contributions, investment returns and cost of running the scheme. If you are to receive a pension benefit under a DC as a lump sum, it would be a total of your contributions, its investment returns less the cost.

DB Pension Fund Value= Total contributions + Returns on Investments – Scheme Charges and Expenses

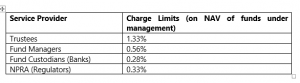

The cost therefore remains a significant factor to retirement incomes. It is important for contributors to know how much they are paying for the management of their fund as part of monitoring the performance of their scheme. Thankfully due to the very sensitive nature of pensions, almost all governments are seen taking very keen interest in the way they are managed. The social price to pay if pensions go pear-shaped is too dear for governments and their politics. Governments empower their regulators to take a keen look. One of the areas looked at is the cost of running a pension scheme. I should say that pensions as a whole enjoys relatively lower charges from service providers due to the social element of the service. The regulations governing pensions in Ghana caps the cost in relation to DC schemes. For contributions into the 2nd and 3rd tier schemes charges are capped at a total of 2.5% per annum of the net value of assets (NAV) under management. The 2.5% per annum total charges are broken down into capped charges for service providers as follows;

There are other costs that would fall outside the stipulated charges and those are to be managed with austerity. Other service providers like auditors have had to significantly discount their regular service charges for pension schemes. Since the charges are on the entire funds, astute management of funds is a must.

Organisations that employ the services of corporate trustees should make sure they have negotiated well. Trustees are also required to do same with other supporting service providers. As an individual within the scheme you could request to see how much you are paying for your scheme and ask questions if need be. This is against the backdrop that scheme costs directly affect the value of the fund and therefore every member’s benefit. Some of us advocate for scheme costs to be brought on scheme statements as a disclosure to contributors. I am sure we would get there some day as part of transparency to contributors. But until that happens you could individually ask and Trustees should make it available to you. It is important as well because pension schemes typically travel for a long time so any ‘mis-charge’ would have a substantial impact on the value of the fund.

For DB schemes like the SSNIT scheme the emphasis is on administrative costs. The lower the administrative costs the better. Cost savings would naturally be ploughed back into the fund to shore liquidity. Their regulations mandate them to charge the ‘appropriate fees’ for services rendered. We hope that SSNIT gets very sensitive to administrative cost to enhance value, and hopefully always remain liquid to fulfill their inter-generational promise of paying current pensioners with taxes from current working generation.

Pension Management Cost is just one of the factors we should look out for as we drive towards our ‘Retiring Richly’ goal.

The author is a Pensions Expert and a Certified Risk Management Professional. You can find his Audio tit-bits on Facebook, Soundcloud and YouTube. Mobile: 0201196080, Email: korankyeyaw2@gmail.com,

{kind=link}