{kind=link}

Below is an extract from Deloitte’s African trends going into 2017 – How business needs to plan for the changing continent report.

The downturn suffered by many African economies following the drop in global commodity prices in 2014 has resulted in a repricing of their economies – with currencies falling against a resurgent US dollar and asset markets, too, tumbling. There is a positive side to this. It could well position them to attract more foreign direct investment (FDI) over the medium term as investors seek cheap assets.

Transmission channels of repricing

The most evident sign of the painful repricing process was that the currencies of many African countries fell heavily. Currencies on the continent have depreciated significantly against the US dollar since 2014 or, in the case of managed currencies, have been devalued. In some cases their value has suffered further as a result of errant monetary policies that have undermined investor confidence and heightened uncertainty.

The exchange rate adjustment has been particularly severe in Egypt, Mozambique, Nigeria, Ghana, Zambia and Angola, where the depreciation against the dollar between the start of 2014 and the end of 2016 has exceeded 40%. Although some currencies recovered to some extent in 2016, this has not been enough to claw back the losses from the earlier falls.

Source: Central banks and Deloitte analysis, 2017

The currency shock has effectively repriced a number of economies. For governments, this has had a severe impact, resulting in rapid fiscal deterioration in many African resource-driven economies.

A key consequence of sharply depreciating currencies (particularly in Nigeria, Ghana, Egypt and, to a lesser extent, Mozambique) is the exacerbation of foreign exchange shortages. As a result, in parallel currency markets that are not controlled by the government, big differentials have opened up with the official rate, as demand for dollars outstrips supply. The large differential between parallel and official exchange rates in countries such as Angola and Nigeria to date suggests that the foreign exchange market is far from reaching equilibrium.

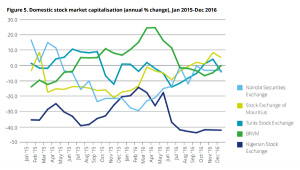

There have also been elements of repricing on stock exchanges across the continent. However, looking at US dollar domestic market capitalisation over the 2014-16 period, there are stark differences when comparing different exchanges. Some have done well.

In the southern Africa region, for example, the Johannesburg Stock Exchange saw an increase of 10.7% from January 2014 to December 2016, while the Namibia Stock Exchange saw its market cap increase by a sharp 40.6% during the same period. Other winners on the continent over the last three years include Morocco’s Bourse de Casablanca (which rose by 7.2%), while the Bourse Régionale des Valeurs Mobilières (BVRM) was little changed, rising by a marginal 0.3%.

READ THIS: The Five Keys to a More Prosperous Africa

In the west African region, however, Nigeria did far worse, with the US dollar market cap of the Nigerian Stock Exchange falling by almost 64% from January 2014 to December 2016. The country’s commercial property sector has also been under pressure, with real estate agencies pointing to over-development and a decrease in corporate demand.

Lagos, Abuja and Port Harcourt’s real estate sector in particular faced pressure during 2016. The vacancy factor index (VFIX) in residential properties in Lagos climbed to 74% in 2016, compared to 63% the previous year.

Furthermore, average office rents in Ikoyi and Victoria fell by 17.6% and 20%, respectively, during the first three quarters of 2016.

These falls create opportunities for longer-term foreign investors, in particular in the Nigerian economy – Africa’s most populous. Assets whose prices were, arguably, highly inflated prior to mid-2014 have become much less expensive.

But foreign investors will also continue to keep a wary eye on the instincts of central banks and government agencies. Foreign exchange shortages in Angola, Ethiopia, Mozambique, Nigeria and Zimbabwe have already resulted in governments tightening foreign exchange rules to protect dwindling reserves. Restrictions have been placed on those who can access foreign exchange, creating so-called ‘captured capital’ that foreign companies cannot repatriate. In the near term, further forex restrictions are likely to be put in place by central banks until foreign exchange reserves start to stabilise again.

Source: World Federation of Exchanges and Deloitte analysis, 2017

Uncertainty in western markets, particularly the extent and scale of fiscal stimulus in the US and the Brexit negotiations between the UK and the EU, are also set to keep markets unsettled. Emerging market currencies tend to suffer in an environment suffused with uncertainty and volatility.

READ THIS: Lessons learned in years of financing African infrastructure

However, the extent of the depreciation in African currencies in the wake of the commodity price slump will provide some protection. Furthermore, increasingly hawkish central banks across the continent should help to bolster African currencies in 2017.

Privatisation opportunities

In order to shore up the balance sheets of governments under increasing fiscal pressure from reduced export earnings and the impacts of currency depreciation, many countries are being forced to embark on long overdue sales of state-owned assets. These programmes typically follow intervention by the IMF. They may herald the beginning of a process not too dissimilar from the one that has either taken place or is now currently occurring in economies such as China and India which in the past had been opposed to private ownership.

While many African governments have been particularly resistant to privatisation, the combination of rising external debt, along with the accompanying interest payments, and weak currencies may force them to sell off assets such as utilities and infrastructure.

Mozambique looks likely to be one such example. To rationalise state spending and reduce fiscal risks, the Mozambican government has approved an independent external audit of public funds and legislation in order to begin reform of public enterprises. More privatisations and the closure or restructuring of public companies are expected.

Source: Deloitte analysis, 2017

Mozambique’s government announced in the latter part of 2016 that it expects to sell (or close) up to 40 state-owned companies. This is viewed as a progressive move for the economy and provides numerous opportunities for firms looking to expand into the country.

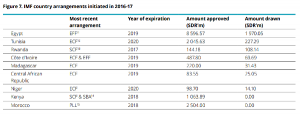

While Mozambique’s fiscal and debt conundrums provide an extreme example, several other countries on the continent are also under strain. IMF involvement in support packages is on the rise and the multilateral organisation is proposing economic restructuring via privatisation.

IMF financial support can come in many forms, although restructuring of inefficient public assets is often a prerequisite. In Zambia, for example, the IMF is calling for the restructuring of the state-owned power utility, Zesco, as part of a proposed US$1.5bn support package.

The IMF has also been involved in Ghana and Kenya for a number of years. In Ghana’s case, the state-owned Electricity Company of Ghana (ECG) is a point of contention, with the Fund advising a shift to independent power producers (IPPs), a reform that trade unions oppose.

In 2016 the IMF provided Kenya, which in 2012 announced the privatisation of 23 state-owned firms, with further access to financial support in its effort to reform the country’s macroeconomy and institutions.

READ THIS: Opinion: Raising Africa’s middle class

Looking ahead, other governments that are not yet under severe fiscal strain are likely to take a closer look at their debt sustainability. This, in turn, may provoke further privatisation.

One country making moves towards privatisation in an effort to promote foreign investment is Ethiopia. The government made an announcement early in 2017 that the country is shifting away from state investment as a means of driving growth and is offering stakes in some state-owned companies to foreign firms. Hailemariam Desalegn, the prime minister, mentioned the state-owned Ethiopian Shipping and Logistics Services Enterprise, but did not provide details on the size of the stake that might be sold. Nor did he mention other state-owned companies that may be privatised. These privatisation efforts are to be commended, particularly if the goal is to drive investment growth, not just shore up government finances.

Credit: Deloitte Team