*South Africa remains the largest FDI hub in Africa

*Egypt, Kenya, Morocco, Nigeria and South Africa (the key hub economies) collectively attracted 58% of the continent’s total FDI projects in 2016

*Investment from the Asia-Pacific region into Africa hit an all-time high in 2016

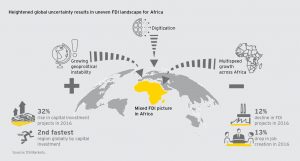

According to EY’s latest Africa Attractiveness report, heightened geopolitical uncertainty and “multispeed” growth across Africa present a mixed FDI picture for the continent.

Download the report here.

The report provides an analysis of FDI investment into Africa over the past ten years. The 2016 data shows Africa attracted 676 FDI projects, a 12.3% decline from the previous year, and FDI job creation numbers declined 13.1%. However, capital investment rose 31.9%.

The surge in capital investment was primarily driven by capital intensive projects in two sectors, namely real estate, hospitality and construction (RHC), and transport and logistics. The continent’s share of global FDI capital flows increased to 11.4% from 9.4% in 2015. This made Africa the second-fastest growing FDI destination by capital.

Ajen Sita, Africa CEO at EY says:

“This somewhat mixed picture is not surprising to us. Investor sentiment toward Africa is likely to remain somewhat softer over the next few years. This has far less to do with Africa’s fundamentals than it does with a world characterised by heightened geopolitical uncertainty and greater risk aversion. Investors with an existing presence in Africa remain positive about the continent’s longer-term investment attractiveness, but they are also cautious and discerning.”

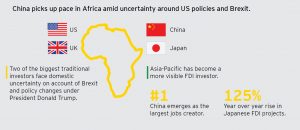

Asia-Pacific investors are bullish on Africa

In a sign of ongoing diversification of Africa’s FDI investors, more than one fifth of FDI projects and more than half of capital investment into Africa came from Asia-Pacific in 2016, an all-time record. Most notably, Chinese FDI into Africa increased dramatically, making the country the single largest contributor of FDI capital and jobs in Africa in 2016.

Foreign investors refocus on Africa’s hub economies

Egypt, Kenya, Morocco, Nigeria and South Africa (the key hub economies) collectively attracted 58% of the continent’s total FDI projects in 2016.

South Africa remains the continent’s leading FDI destination, when measured by project numbers, increasing 6.9%. Morocco regained its place as Africa’s second largest recipient with projects up by 9.5%, followed by Egypt, which attracted 19.7% more FDI projects than the previous year.

New investment hubs appear in East and West Africa

Although foreign investors still favour the key hub economies in Africa, a new set of FDI destinations is emerging, with Francophone and East African markets of particular interest.

Despite having a 31.7% decline in FDI projects in 2016, and weak growth in recent years, West Africa’s second largest economy, Ghana, remains a key FDI market. The country’s improving macro-economic environment and strong governance track record has seen Ghana rise to fourth position in the EY Africa Attractiveness Index (AAI). The index was introduced in 2016, to measure the relative investment attractiveness of 46 African economies based on a balanced set of shorter and longer-term metrics.

Staying in West Africa, Cote d’Ivoire also features in the top 10 of the AAI, and with a 21.4% jump in FDI projects in 2016, this illustrates that it’s becoming a country more favoured by investors.

Also in the west, Senegal has emerged as a potential major FDI destination although this is not reflected in its current FDI numbers. It does however rank strongly on the AAI 2017, taking eighth position, due to its diverse economy, strong strides in macro-economic resilience and progress in improving its business environment.

Sita concludes, “By 2030, Africa remains on track to be a US$3t economy. However growth needs to become more inclusive and sustainable to eradicate poverty at the levels that are required. If we accept the reality that physical connectivity – enabled by regional integration and the development of physical infrastructure – will remain a key stumbling block to inclusive growth across Africa for at least the next decade, then the need to actively embrace digital connectivity becomes critical. However, efforts to harness the potential of digital technologies as a fundamental driver of inclusive growth are still far too piecemeal and fragmented.

What is required is a far more collaborative effort between governments, business and non-profit organisations to adopt technological disruption, and create digitally enabled offerings with a particular focus on health, education and entrepreneurship.”

{kind=link}